ACA 1095 Forms

1095 forms, 1094 transmittals and envelopes for ACA reporting of health insurance coverage for employees.

- ACA Compliant 1095 forms

- 1095-B and 1095-C forms

- 1094 Transmittal forms

- Low minimum quantities

- Fast shipping and friendly service

- 1095 Software and Online 1095 Form Filing are also available

Easy printing and mailing with the right ACA 1095 forms and options for compliant health coverage reporting.

Shop easy, ship fast with The Tax Form Gals!

ACA 1095B Forms

1095-B Forms for Self-Insured Employers and Insurance Companies

-

Blank Pressure Seal 1095 Forms – 14″ EZ Fold

-

1095 Envelopes for ComplyRight Format Forms Only

-

1095 Blank Paper with Instructions

-

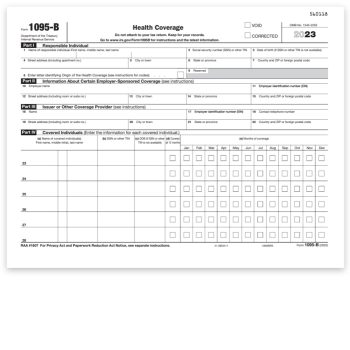

1095-B Forms – IRS Half Sheet Format

-

1095-B Forms – ComplyRight Format

-

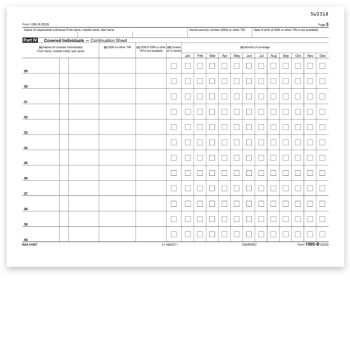

1095-B Continuation Forms – IRS Half Sheet Format

-

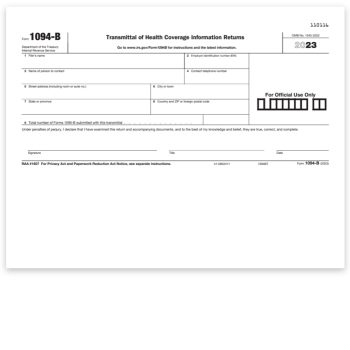

1094-B Form – Transmittal

-

1095 Envelopes for Other Software

-

1095-B Continuation Forms – ComplyRight Format

ACA 1095C Forms

1095-C Forms for Employers with 50+ Full-Time Employees

-

Blank Pressure Seal 1095 Forms – 14″ EZ Fold

-

1095 Envelopes for ComplyRight Format Forms Only

-

1095 Blank Paper with Instructions

-

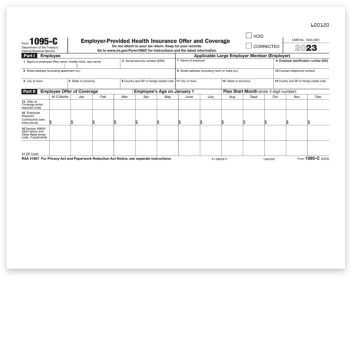

1095-C Form – IRS Half Sheet Format

-

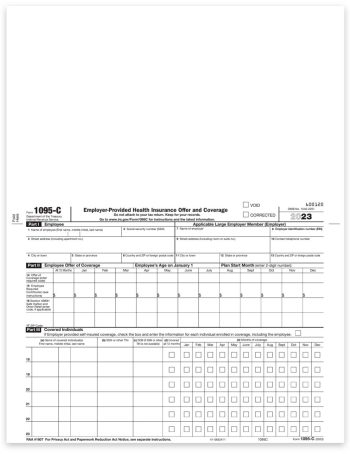

1095-C Forms – ComplyRight Format

-

Pressure Seal 1095-C Form – 14″ EZ Fold

-

1095-C Dependent Continuation Forms – IRS Half Sheet Format

-

1094-C Form – Transmittal

-

1095 Envelopes for Other Software

-

1095-C Continuation Forms – ComplyRight Format

Online Filing Eliminates the Forms!

ACA 1095 Filing Requirements for Healthcare Insurance Coverage Reporting

As part of the Employer Shared Responsibility Rule of the Affordable Care Act (ACA), 1095 forms are required to be filed by employers and insurance companies to report individual health care coverage during a tax year.

Medium-to-large size businesses and health insurance companies need to file 1095 forms.

Who exactly needs to file:

- Employers with 50+ full-time employees (or full-time equivalent)

- Self-insured employers with fewer than 50 employees (a very small number of businesses)

- Health insurance companies

- Businesses can file these forms themselves, or outsource to a payroll company.

Forms 1095-B and 1095-C are used to report coverage information to the IRS and employees.

1095 forms include the following information:

- Enrolled employees and former employees

- Details of employees’ health insurance coverage

- Verification that the minimum essential coverage (MEC) requirement has been met.

Employees and their dependents will use this information to complete their personal tax returns – and those who do not have minimum essential coverage may receive a penalty on their tax returns.

1095-C is for applicable large employers with 50+ full time employees

1095-B is for self-insured employers and health insurance companies

1094-C and 1094-B are the summary transmittal forms

1095 forms must be filed with the IRS on paper or efile, and also provided to the employee.

Form | What's Reported | Who Issues | Submit to IRS? | Recipient Copies? |

1095-B | Which months the insured and their family was covered under the plan. | Self-Insured Employers, with fewer than 50 full-time employees, that provides health insurance plans. | Feb. 28 paper; | Yes, by Jan. 31 |

1094-B | Summary transmittal record of | Accompanies 1095-B forms when mailed to the IRS. | Feb. 28 paper; | n/a |

1095-C | Whether or not the employer offered health insurance coverage to employees. | Employers with 50 or More Full-Time Employees (applicable large employers). Both insured and self-insured issue 1095-C | Feb. 28 paper; | Yes, by Jan. 31 |

1094-C | Summary transmittal record of | Accompanies 1095-C forms when mailed to the IRS. | Feb. 28 paper; | n/a |